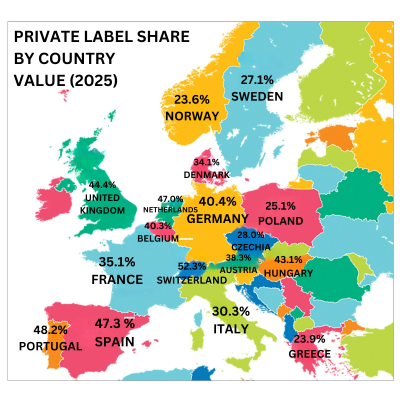

Private label continued its strong momentum across Europe in 2025, reinforcing its role as a strategic pillar for retailers and a key growth engine for manufacturers. According to to the latest data from NielsenIQ, total private label sales across 17 monitored European markets reached €387 billion, up €15.3 billion, giving store brands a 38.8% share of the grocery market.

Growth once again outperformed the broader grocery sector. Private label turnover rose 4.1%, compared with 3.2% growth for the total market and 2.7% for manufacturer brands. In volume terms the gap was even clearer: private label unit sales increased 1.3%, more than double the overall market’s 0.6%, while branded products saw a slight decline.

Inflation and heightened price awareness continue to influence shopper behaviour, but value alone does not explain the success of private label products. Retailers have increasingly invested in innovation, product quality and sustainability to strengthen the value proposition of their brands and build consumer trust. According to research by Euromonitor International, retailers are embedding sustainability and product innovation into private label development to position their own brands as credible and value-driven competitors to national brands.

Despite this progress, Europe remains a highly diverse landscape. Private label now exceeds 50% market share in Switzerland, while in the other countries value shares range from 48.2% in Portugal to 23.6% in Norway. In 12 of the 17 countries analysed, private label grew faster than branded goods in 2025. The strongest growth markets were Portugal, Hungary, Norway, Spain and Greece, highlighting opportunities in markets where retailer brands are still expanding.

Performance also varies by department. Private label growth was particularly strong in health care, where sales rose 13% in value and 10% in volume, albeit from a small base. Meanwhile, fresh and perishable foods continued to perform well, reflecting rising consumer demand for healthier and more transparent food options.

Consumer perception is also shifting. Surveys show that 96% of shoppers consider private label essential to their shopping basket, with most believing store brands now match national brands in both quality and sustainability.

The overall picture is clear: Europe’s grocery markets may differ widely in structure and maturity, but across this mosaic of markets, private label is firmly embedded and continuing to grow.

To actually see, experience, and exchange ideas about the latest developments in private label make sure you attend the 2026 “World of Private Label International Trade Show in Amsterdam on 19-20 May, and the pre-show seminars on 18 May. Click here to register.

“A mosaic of markets: PLMA’s 2026 Report on the status of private label across Europe” will soon be available, check the website www.plmainternational.com.